.

Can Facebook, Instagram, Twitter, all of the cars on the train survive the crash?

Disruptive Innovation and Social Media, a Signature Presentation

Paradigms are meant to be replaced. The

phenomenon known as "social media" may or may not be considered a

paradigm in the strict sense of the word but it has made a major mark not just

on the internet but on culture itself.

Within the confines of the social media

universe, trends rise, and fall depending on the demands made by consumers and

demands developed by industry. Pressure from both of those demands creates an

atmosphere where progress, often times radical, replaces inertia. That pressure

in radical form is defined by Clayton Christensen of Harvard University as

"disruptive innovation."

“Disruptive innovation” was outlined in

the Jill Lepore 2014 article in The New Yorker titled “The Disruption

Machine.” Citing one of her associates

at Harvard, Clayton Christensen, she defined disruptive innovation as;

“The selling

of a cheaper, poorer quality product that initially reaches less profitable

customers but eventually takes over and devours an entire industry.” (Lepore,

New Yorker)

Curiously, Lepore goes on to report that a company using the

disruptive innovation paradigm will have to fail in order to succeed. She cites

Morrison-Knudsen's effort for mass transit which resulted in total failure of

the company.

By his own

account, the founder of Friendster, Jonathan Abrams, blames venture capital for its failure.

Another entrepreneur, Joel Spolsky, has it right when he says;

"The basic venture capital system

is structured so that there are built-in conflicts of interest between the VC

and the entrepreneur," (Max

Chafkin, inc.com)

The market for upstart social media networks in the days of

Friendster survived in a narrow range and investors hedged their bets by

spreading cash out across the board. Naturally, when a better platform

surfaced, the money went there, and Friendster was relegated to the dustbin of

history; the first disruptive innovation in social media had failed. That, in fact, is the paradigm we are

looking for in whether a social media endeavor, or social media itself, will survive

in cyberspace, where survival of the fittest is the bottom line, and money is

what fuels it.

Fast forward to the current status quo

of the primary social-media platform, Facebook (NYSE:FB). The company went

public in May of 2012. It's current stock value is just under $200 a share. Its

primary source of revenue is, not being liked by everyone posting pictures of

their pets or trip to Paris, but advertising.

By the 4th quarter of 2018, the revenue topped just over $16 billion,

most of which were publishers from the United States. Facebook depends on its

US advertising to survive, there is no diversification, a basic component to

stay in business in America. (Statista)

According to

Statista, the United States does not lead the world in Facebook users, but it

is India, a predominant market in what Dr. Pain of the Reynolds School of

Journalism at the University of Nevada, Reno, refers to as "The Global

South." (Statista) Facebook is

still a one-trick pony depending chiefly on running ads to generate revenue

basing its success on the number of users on the platform, but that's changing;

"...despite Facebook’s advertising growth, its user

growth rate slowed during the quarter. The social network only added 38 million

new monthly active users during the quarter. " (Digital Commerce 360)

Now that we have

set the stage for the crash, let's examine the mechanics. The above might be

considered the hard scientific data on the current state of social media. We

might call it a synthetic, or an inductive, interpretation. What about the

analytical, or deductive interpretation? That's where we can see the weakness

in the system, and it goes back to what happened to Friendster. The evolution

from that site through the rise of Myspace to the eventual social media

pinnacle established by Facebook is no matter of personal privacy, everybody

knows about it. The difference was that Myspace never went public and was

bought out by NewsCorp in 2005 (NAS:NWS);

"News had

been looking for $100m but settled for $35m offer from advertising targeting

firm Specific Media. The sale is believed to be mainly in stock and News Corp

will retain a small holding." (The Guardian)

Of course, what else would the site be good for but to run

ads, just like the rest of the social media platforms that have no diversified

material products to sell. This brings us back to deducting just what the flow

chart looks like to the eventual decline of Facebook itself. Consider two

things, where the revenue is coming from to float its income and who are the

venture capitalists behind the wall propping it up.

First, the graph

shows half its income is in the US-Canada market, which makes sense because

that's where the money is. That's who can afford to promote their favorite pet

or trip to Paris video on mobile phones. The problem isn't how much Facebook

rakes in on the successful market, but its limited returns in The Global South.

The largest prospect for growth is there, as seen in the explosion of users

from India; even though the prospect to find ad publishers is very limited. No

matter many people Facebook has coming into the site, if the money isn't there

to support them, the stress will fall on the infrastructure. (Graph, Merch

Today)

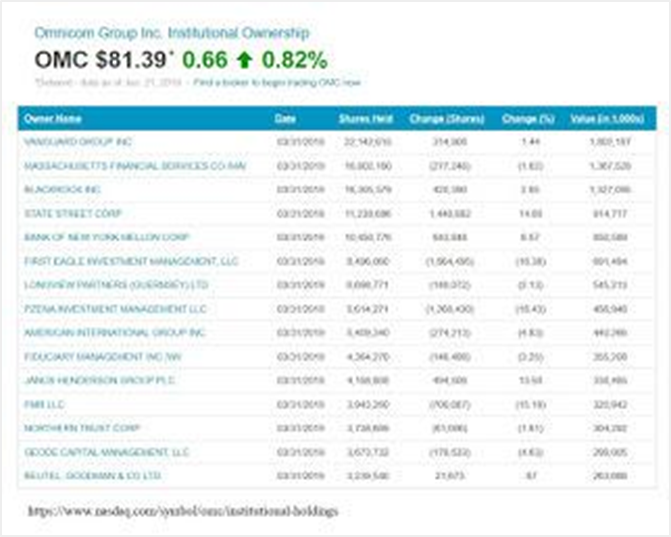

Footing the bill

for the stock is Vanguard Group out of Pennsylvania, one of the largest funds

in the world. Its portfolio is spread across a myriad of sectors but its top

holdings fall into a limited category, with ten out of top twenty stocks on the

Dow Jones Industrial Average of 30 stocks. Even though there is a strong tech

presence in the top twenty, it all about drugs, and it always is. Three of

those are on the Dow30, Proctor & Gamble (NYSE:PG), Johnson & Johnson

(NYSE:JNJ) and Merck (NYSE:MRK).

(Nasdaq) Keeping with the theory that venture capital spreads cash

across the sector, betting big in hopes another Google (NAS:GOOG) will surface

from the faces in the crowd, Vanguard is also the principal investor in Omnicom

(NYSE:OMC). (Nasdaq) OMC is one of the

largest ad agencies in the world and even though its venues are different, it

stands in direct competition with Facebook for consolidating the worldwide

advertising publishing market. They are on a collision course, in effect, a

head-on train wreck.

When the crews

clear the debris, it will be clear OMC survived due to a given number of

basics, depending on global reach across a wide variety of venues,

diversification in content, the ability to undercut the cost, and add to that

the variability of clients it can attract for advertising. As FB revenues

decline, Vanguard will opt to keep its particular portfolio in the sector

balanced and the money will go not just to OMC but others who, as disruptive

innovation requires, will emerge from the rubble. The timeline, as in any good

deductive inquiry, is always up for speculation.

It depends on the

market as a whole, global pressure on the survival of social media as a

bona-fide cultural necessity, emergence of it in regions such as the poorer

Global South and the ability of those in the sector to support the

infrastructure required to keep it online. There are the other usual

restrictions, such as political, as seen every time some general decides he

wants to topple a Third World country in a coup and an internet blackout is

ordered with surveillance and shutting down of social media to contain

organizing and dissent. Can Facebook, Instagram, Twitter, all of the cars on

the train survive the crash?

Credits:

Disruptive Innovation, Lepore, Jill, The Disruption Machine,

2014, https://www.newyorker.com/magazine/2014/06/23/the-disruption-machine

Chafkin, M., Friendster, How to Kill a Great Idea, https://www.inc.com/magazine/20070601/features-how-to-kill-a-great-idea.html

FB Revenue, https://www.statista.com/statistics/218701/largest-source-of-revenue-of-leading-tech-companies/

FB Growth, https://www.digitalcommerce360.com/2018/07/25/facebooks-ad-revenue-jumps-42-in-q2/

MySpace, https://www.theguardian.com/technology/2011/jun/30/myspace-sold-35-million-news

FB Revenue Graph, https://martechtoday.com/despite-ongoing-criticism-facebook-generates-16-6-billion-in-ad-revenue-during-q4-up-30-yoy-230261

Vanguard Top, https://www.nasdaq.com/quotes/institutional-portfolio/vanguard-group-inc-61322?sortname=sharesheld&sorttype=1

OMC Investors,

https://www.nasdaq.com/symbol/omc/institutional-holdings

Disruptive Innovation and the Crash of Social Media: first published in 2019.